Japanese Home Contents Insurance Explained (2026)

June 28, 2026 | Family Life | Japanese Best

Most overseas residents in Japan discover home contents insurance by accident—usually after mentioning a flooded apartment or broken window to a Japanese colleague, only to hear, “Ah, you need kasai hoken.” It’s a system that quietly underpins how Japanese families protect their lives, yet remains largely invisible to those unfamiliar with Japan’s insurance culture. Understanding home contents insurance reveals something deeper about Japanese domestic life: how families balance risk, community norms, and practical preparedness in a country prone to earthquakes, typhoons, and tight urban living. This guide covers what Japanese home contents insurance actually pays for and what it costs.

Quick Summary

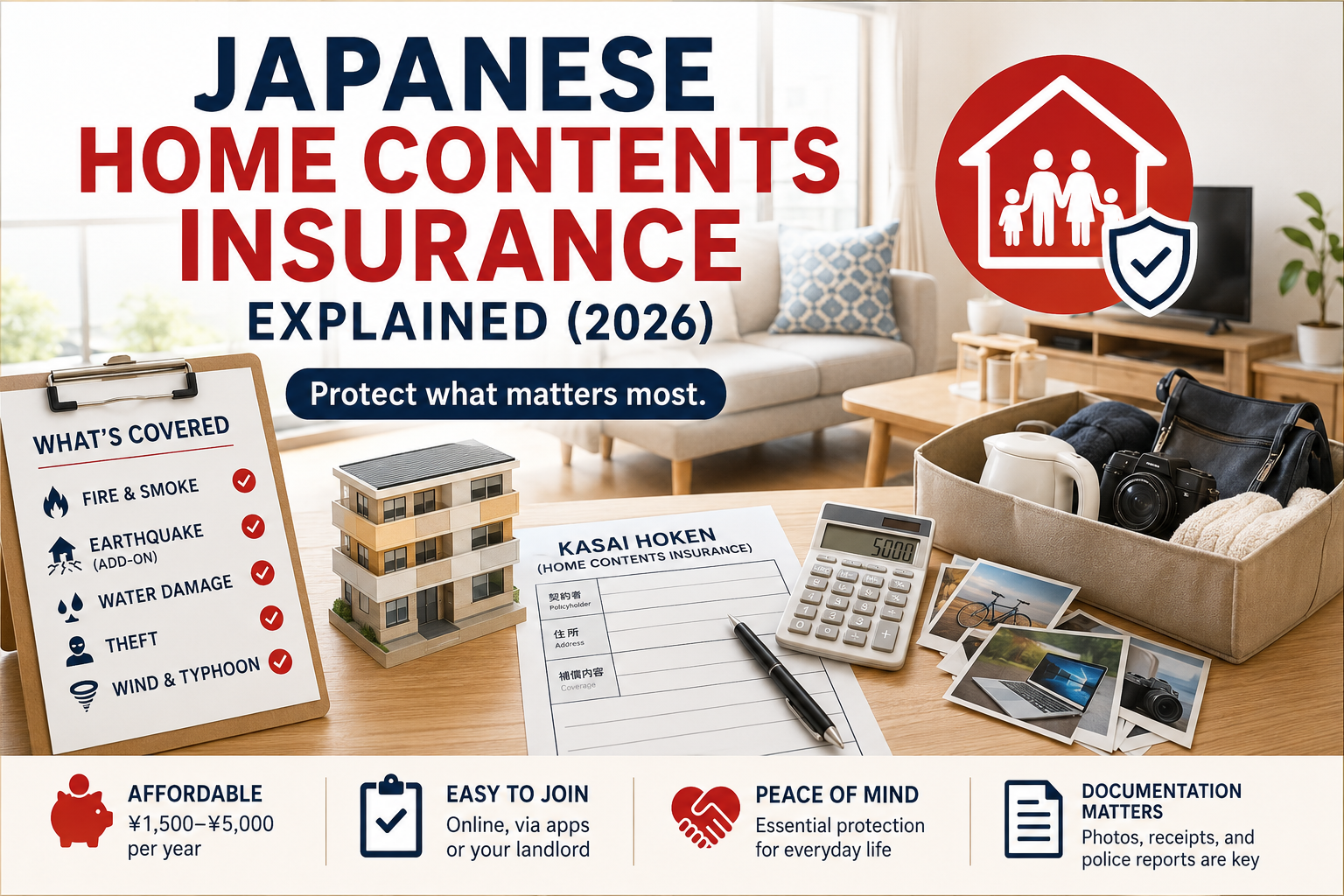

- Home contents insurance (kasai hoken) covers belongings inside your home, not the structure itself—that’s the landlord’s responsibility in rental properties

- Premiums are typically ¥1,500–¥5,000 annually for renters in major cities, making it affordable for most households

- Earthquakes, fire, theft, and water damage are standard coverage, though earthquake coverage often requires a separate add-on

- Japanese families treat it as essential, much like health insurance, not an optional extra

- Claims are straightforward but require documentation—photos, receipts, and police reports for theft create a paper trail Japanese insurers expect

🛒 Shop Recommended Products

The Basics: How Home Contents Insurance Works

Home contents insurance in Japan—kasai hoken (火災保険)—protects your personal belongings rather than the building itself. For renters, which describes roughly 40% of Tokyo’s population, this distinction matters enormously. Your landlord or property management company holds building insurance; you protect what’s inside: furniture, electronics, clothing, and kitchenware.

Most Japanese families shop through major insurers like Sompo Japan, Tokyo Marine, or Zurich, often comparing quotes online through aggregator sites. A typical renter in central Tokyo pays ¥2,000–¥3,500 annually for basic coverage. Families with higher-value contents—art collections, designer furniture, or expensive electronics—pay more. Homeowners purchase broader policies covering both structure and contents, typically costing ¥4,000–¥8,000 yearly. For background on the industry itself, see the General Insurance Association of Japan.

The cultural norm is clear: you insure. Japanese friends will ask whether you’re covered before discussing any household mishap, treating it as a basic responsibility like paying utilities. Insurance companies distribute pamphlets in apartment buildings, and real estate agents routinely recommend policies when you sign a lease. It’s woven into the fabric of responsible adult life.

A Typical Week / Month

During an ordinary month, a Japanese family’s relationship with home contents insurance remains passive—premiums auto-debit from a bank account, usually on the 1st or 15th. But insurance sits in the background of everyday decisions.

When a family in Shibuya orders a washing machine online, they might choose delivery insurance. When a Kyoto householder learns heavy rain is forecast, insurance awareness surfaces. Parents in earthquake-prone prefectures discuss coverage annually before typhoon season (September–October). Some families photograph valuable items yearly, creating an inventory that proves ownership if disaster strikes.

The real engagement happens when something actually happens. A burst pipe floods a Yokohama apartment; the tenant calls the insurer’s 24-hour hotline, files a claim within days, receives an adjuster’s visit, and within two weeks gets a payout. Or a bicycle is stolen in Osaka; the family files a police report (mandatory for theft claims), submits it to the insurer, and receives reimbursement. These moments—usually stressful—become far less chaotic because the system expects documentation and responds predictably.

What This Looks Like in a Real Tokyo Home

Imagine a young couple, Yuki and Hiroshi, living in a 2LDK apartment in Chiyoda ward. They pay ¥2,200 monthly rent and chose a home contents policy covering ¥2 million in belongings for ¥2,800 annually. Their policy covers fire, theft, water damage, and storms—standard inclusions.

When a typhoon damaged their balcony door and rain soaked their living room in August, they called their insurer’s emergency line immediately. Within 24 hours, a damage assessor visited, photographed everything, and explained the claims process. Three weeks later, they received ¥380,000 to replace their sofa, television, and flooring. The process felt reassuringly bureaucratic: forms, timestamps, receipts—very Japanese.

Yuki also pays extra for earthquake coverage (¥1,200 additional annually), something many younger Tokyoites do since the 2011 Tōhoku disaster reshaped national awareness. Their policy excludes valuables left in obvious places (like money on the kitchen table) and requires locks on windows for theft claims. This specificity—these particular rules—is typical. Japanese insurers are meticulous about conditions and exclusions, expecting customers to understand them fully.

How It Differs From Other Countries

Japanese home contents insurance feels distinctly Japanese in its rigour and specificity. Unlike some American policies bundled with renters’ or homeowners’ insurance, Japanese kasai hoken is typically purchased separately and treated as its own responsibility. There’s no cultural assumption that your landlord’s building insurance covers your belongings—that’s explicitly your concern.

British readers will recognise similarities to UK home contents policies, but Japanese insurers demand far more documentation. Submitting claims without photos, receipts, or police reports (for theft) is virtually impossible here. This isn’t bureaucratic obstruction; it reflects Japan’s broader insurance culture, where precision and evidence prevent fraud and expedite payouts.

Claims payouts in Japan also operate on a slightly different timeline. Rather than settling claims in days, insurers typically take 2–4 weeks, conducting thorough assessments. For someone accustomed to faster Western processes, this feels slow—but for Japanese families, it feels normal and trustworthy.

Related Products

If you’re concerned about protecting your home contents in Japan, air quality matters too. Many Japanese families, particularly those in urban areas, invest in air purifiers alongside insurance. The Panasonic F-VXR70 nanoe X Air Purifier uses advanced nanoe X technology to target airborne pollutants and allergens—important for protecting the items you’re insuring, and your family’s health. Alternatively, the Sharp FP-J80-W Plasmacluster Air Purifier actively disperses ions to neutralise airborne irritants, a popular choice in Japanese households concerned about indoor air quality.

FAQ

Do I need home contents insurance in Japan if I’m renting?

Legally, no—but most landlords expect it, and it’s genuinely sensible protection. Many lease agreements list it as a requirement.

What if I own my home, not rent?

You’ll purchase a broader policy covering both the structure and contents, costing more but offering complete protection.

Can I claim for theft without a police report?

No. Japanese insurers require a formal police report (keisatsu chōsa) for any theft claim. File it immediately.

Are natural disasters always covered?

Fire and storms are standard. Earthquakes usually require paid add-ons—¥1,000–¥2,000 extra annually—which many families choose in earthquake-prone regions.

What if I move apartments?

You’ll need a new policy for your new address. Most insurers cancel the old one pro-rata and issue a new quote.

Home contents insurance in Japan embodies the country’s pragmatic, meticulous approach to shared risk. It’s neither glamorous nor complicated, but rather a quiet assurance that everyday disasters won’t become financial catastrophes. For overseas residents, understanding kasai hoken means understanding how Japanese families think about security, responsibility, and preparedness—values that extend far beyond insurance documents into the way they live.

Seen in Everyday Life in Tokyo

A Real-Life Note from Japan

What I Often See in Japanese Stores

Related Japanese Products

The products below came up naturally in the context of this article. We only recommend items that genuinely connect to the topic.

| Product | Brand | Best For | Amazon |

|---|---|---|---|

| Panasonic F-VXR70 nanoe X Air Purifier | Panasonic | Families concerned about allergens, pollen, and indoor air quality in Japanese cities | Search on Amazon |

| Sharp FP-J80-W Plasmacluster Air Purifier | Sharp | People who want an active air purification approach rather than just passive filtration | Search on Amazon |

Panasonic F-VXR70 nanoe X Air Purifier

Panasonic’s top-of-line air purifier with nanoe X technology targets viruses and allergens.

Best for: Families concerned about allergens, pollen, and indoor air quality in Japanese cities

Sharp FP-J80-W Plasmacluster Air Purifier

Sharp’s Plasmacluster ion technology actively disperses ions to neutralise airborne pollutants.

Best for: People who want an active air purification approach rather than just passive filtration

More From Japanese Best

Disclosure: As an Amazon Associate, Japanese Best earns from qualifying purchases. This does not affect our recommendations. We only feature products we genuinely believe are worth your consideration.

Editorial Disclaimer

The views, opinions, and recommendations in this article are the author’s own and reflect personal experience living in Japan. They do not constitute professional, financial, or purchasing advice of any kind.

Product availability, pricing, and specifications are subject to change without notice. Japanese Best makes no warranties — express or implied — regarding the accuracy or completeness of this content, and accepts no liability for any decisions made based on it. Always verify details directly with the retailer or manufacturer before purchasing.

コメント